As consumer behavior rapidly shifts toward more flexible and varied POS financing options, banks recognize that they need to expand beyond their traditional lending models and diversify their lending products and offers. Partnering with a fintech technology provider like ChargeAfter’s Lending Hub is pivotal for banks to succeed.

The Lending Hub offers a comprehensive all-inclusive embedded lending platform for banks to create, manage, and distribute a wide range of POS financing products – from consumer finance with revolving lines of credit, short and long-term installments, BNPL, and personal lending. By adopting such diversified offerings, banks can cater to the nuanced and evolving needs of modern consumers, enhancing customer satisfaction and loyalty.

Challenges addressed by ChargeAfters’ Lending Hub

One of the significant challenges faced by banks is the complexity of merchant onboarding and integration. ChargeAfter’s Lending Hub simplifies this process through its robust enablement tools and streamlined merchant onboarding protocols, reducing operational costs and time and increasing merchant satisfaction. This approach not only accelerates market entry but also establishes a stronger network of merchant partnerships, essential in today’s competitive environment.

The Lending Hub also addresses crucial aspects like the protection of Personally Identifiable Information (PII). In an era where data security is paramount, ChargeAfter ensures compliance with the highest standards of data protection, giving both banks and their customers peace of mind.

As shopping behaviors evolve, banks need to adapt to the natural evolution of shopper needs. ChargeAfter’s Lending Hub enables banks to stay ahead of the curve, offering tailored POS financing solutions that resonate with contemporary consumer demands. This adaptability ensures that banks remain relevant and competitive.

The technological backbone of ChargeAfter’s Lending Hub aligns perfectly with the banking core architecture. By leveraging cloud-based hosting and microservices, the platform ensures scalability, security, and operational efficiency. This infrastructure supports an agile development process, allowing for rapid deployment and continuous improvement of financial products. This agility is vital in a financial world that demands quick adaptation to market changes and consumer trends.

Partnering with ChargeAfter’s Lending Hub is not just about offering a range of financial products; it’s about embracing a holistic, future-forward approach to banking. It’s about meeting the needs of today’s consumers with innovative solutions and cutting-edge technology. As banks look towards a new era of digital finance, ChargeAfter stands as a valuable ally in navigating this journey together.

Jeffrey Tower EVP Global Business Development Jeff has over 20 years of experience driving revenue through building global brand awareness, business development, marketing, and sales departments focused on consumer financing, fintech, and eCommerce.

We are delighted to share that ChargeAfter has received the award for “Best Banking Services Provider” in Furniture Today’s 2023 Reader Rankings. Additionally, we were named a “Best Consumer Finance Company” finalist.

The Furniture Today Reader Ranking awards are a celebration of excellence within the furniture industry. They hold special significance as readers nominate and vote for each award. The recognition underscores the value we bring to merchants by helping them seamlessly provide personalized financing choices to their customers at every point of sale. This acknowledgment reflects the appreciation of those within the furniture industry who understand the impact of our embedded lending platform in boosting approval rates, building brand loyalty, and increasing sales conversion. We want to say a big thank you to everyone who voted for us!

It is also significant that our fellow finalists and winners of these two awards are our lending partners, confirming what we already know – that we are working with the best of the best! Congratulations to Wells Fargo, Synchrony, and Koalafi and the winners and finalists in every category.

When it comes to evaluating a POS lender for your business, merchants, service providers, and contractors typically focus on two metrics – approval rates and cost.

Pricing is straightforward to assess, but what about approval rates? Are they a reliable metric for comparing financing programs?

While approval rates are essential, they are only part of the story. If upgrading your point-of-sale financing experience is on your agenda, there are additional factors that you should consider to evaluate finance providers uniformly.

POS financing approval rates

Approval amount

Loan terms & conditions

Does the financing amount offered meet the sale amount

A summary of each is provided below.

POS Financing Approval Rates

What does it mean if a point-of-sale finance provider indicates they have an approval rate of 80%? Are they referring to ecommerce applications? Perhaps they are talking about in-person or in-store applications. The consumer finance provider likely has different underwriting strategies for each channel that affect approval rates for that channel. Given this complexity, a better indicator would be approval percentages by consumer fico tier and channel(s) as appropriate.

Approval Amount

Another important factor when selecting a consumer lending partner is whether their minimum and maximum loan amounts align with your ticket requirement. For example, if your average ticket is less than $300, you are probably focused on BNPL providers. If the average ticket is $3,000, deferred interest options like 0% interest and extended terms will be critical.

Loan Terms & Promotions

The most popular POS lenders bring extra value to the table beyond just cost, approval rates and approval amounts. These providers act as a cousultant and advise you about trends and best practices in consumer finance. Consider the added value of a partner that can explain the benefits of a deferred interest program versus equal payments with no interest or why installment loans might be better than revolving lines of credit for your customers.

Financing Offered Meets the Sale Amount

This is one of the most critical, but often overlooked, metrics when choosing the best lending partner for your business.

You need to understand the percentage of the lender loan offers that equals or exceeds the purchase amount requirement. Having a high approval rate is great, but what good is a loan offer that doesn’t allow the consumer to make the purchase? For example, how helpful is it to offer your customers a $1,500 loan when trying to sell a treadmill for $2,500?

Purchase Conversion Rate

The Purchase Conversion Rate is arguably the most important metric and answers whether a finance program will drive sales.

The conversion rate is the percentage of offers accepted by the consumer and utilized to make a purchase. Factors that impact conversion rate can include:

Is the consumer redirected from the merchant website to apply?

Is there a seamless transition from one program to another if the consumer is declined?

Are the repayment terms and conditions agreeable?

If the consumer experiences friction anywhere in the purchase process, they are more likely to drop out and abandon the cart. A seamless customer journey with agreeable terms and conditions is more likely to result in a purchase.

The Embedded Lending Platform Advantage

One of the major advantages of ChargeAfter’s embedded lending platform is the ability to provide merchants with these analytics and much more. Merchants can view the performance of each lending partner in a single console and on a near real-time basis.

With this data, merchants are empowered with the tools they need to better evaluate the performance and effectiveness of their lending partners, identify any gaps in consumer coverage, evaluate new promotion offers, and even perform A-B testing with various lenders.

ChargeAfter operates the largest network of lending partners offering installment loans, private label credit cards, revolving lines of credit, BNPL, subprime lending, lease-to-own, and even B2B financing. A single integration with ChargeAfter provides you with access to all of the programs and tools you need to maximize finance penetration.

Kevin has worked in the banking and finance industry for over a decade. He has worked closely with some of North America’s largest banks, financial institutions, and retailers. Kevin is an expert in embedded consumer financing and B2B financing and has a deep understanding of current trends and where the industry is heading.

In today’s fast-paced retail environment, ensuring customers have seamless access to financing choices is critical to boosting sales and building customer loyalty. The ability to pay for goods over time through financing can be the deciding factor when completing a purchase. This is especially true during this period of inflation when people are more protective of their resources. Even without inflation, consumer demand for financing is likely to continue as credit cards drop in popularity with younger generations.

One of the consequences of the rise of demand for consumer financing is that it has become impossible for merchants to create and manage an exceptional financing offer in-house. To manage a robust financing offer, retailers require a technology partner to integrate point-of-sale financing into modern customer journeys. This solution is best provided by a platform that can meet the needs of diverse customer profiles while being fast and easy to use for customers and merchants alike. Implementing the right consumer financing platform has become a strategic must for merchants.

For leading merchants, ChargeAfter is the platform of choice. Here are seven reasons why.

7 Reasons Why Leading Merchants Choose ChargeAfter

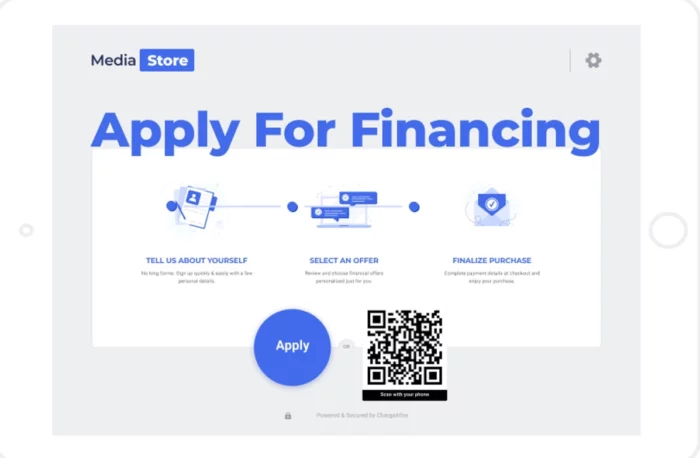

Your customers expect a seamless, omnichannel purchasing experience, especially for big-ticket items. Some customers start their purchasing journey online before heading to a brick-and-mortar store or interacting with a call center. Your financing offer must be embedded into these omnichannel journeys. Your offer must also be flexible enough to meet your and your customer’s needs and not be tied to rigid experiences, such as in-store stands serving a long line of customers.

ChargeAfter enables this with a state-of-the-art customer-facing application. It makes it easy for you to offer different ways to access financing choices at every point of sale. This can include a QR code in-store or online, sending customers a link to apply, promotional links on your eCommerce site, online pre-approval, and in-store devices – whatever works best for you and your customers.

Expansive Network of Lenders

With over 40 lenders embedded into ChargeAfter’s platform, you can easily offer your customers access to diverse financing products that to cater to every consumer, regardless of their financial standing. As a result, your approval rates are likely to increase to up to 85%.

Especially during economic fluctuations, having a diverse range of lenders, including B2B financing options, ensures every customer is included. The platform also offers merchants the flexibility to introduce their preferred lenders. Such an expansive network ensures that you remain resilient against individual lender decisions and allows you to capitalize on every sales opportunity.

Easy Integration with Waterfall Finance Methods

The platform stands out with its simplicity. Merchants can enjoy easy integration of this embedded finance platform into their systems. ChargeAfter uses a waterfall finance method that instantly matches customers with the best lending offers suited for their credit profiles. Additionally, its post-sales management features—dispute resolution, refunds, and reconciliations—provide real-time insights. Such embedded financing ensures that merchants and consumers can transact with ease and speed.

Customize with White Label Consumer Financing

ChargeAfter’s white-label POS system allows customization for businesses prioritizing brand identity, reinforcing brand loyalty. Whether you’re seeking a white-label BNPL solution or comprehensive white-label consumer financing, ChargeAfter has you covered.

Unwavering Compliance and Security

Data security, especially in e-commerce financing, is paramount. ChargeAfter’s commitment to both transactional and personal data security is exemplary. Their platform ensures that every piece of data, from credit details to personal identifiers, is guarded against potential breaches. Furthermore, they adhere to all financial regulations, both federal and local. This commitment to embedded finance solutions, combined with unwavering security protocols, ensures merchants can focus on selling, free from the hassle of intricate financial regulations.

Higher Approval Rates Equate to Increased Sales

Through its multi-lender setup, ChargeAfter revolutionizes POS financing. With a broader spectrum of lenders, consumers enjoy a higher likelihood of loan approval, motivating them to finalize their purchases. This embedded lending approach ensures sales and makes your offerings more accessible to a broader audience.

Actionable Analytics and Data

Data-driven insights are crucial for improving customer experiences and optimizing sales strategies. ChargeAfter offers comprehensive analytics, allowing merchants to understand their customers’ buying journeys. Whether it’s identifying drop-off points or successful conversion moments, these insights enable the optimization of the POS lending process.

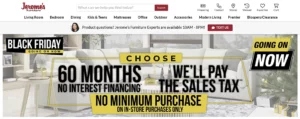

Case Study: Jerome’s

The success story of Jerome’s Furniture, a legacy brand with over six decades of experience, has been profoundly enriched by its partnership with ChargeAfter. Jerome’s astute integration of ChargeAfter’s consumer financing platform showcased how forward-thinking strategies can lead to exponential growth, even during economic uncertainties. With a commendable 67% increase in customer financing adoption, Jerome’s has ensured its clientele can afford quality furniture without financial strain. This case study underscores the pivotal role consumer financing plays in modern retail, exemplifying how strategic collaborations and a focus on customer-centric solutions can yield impressive outcomes.

Want to delve deeper into Jerome’s Furniture’s remarkable growth journey with ChargeAfter? Download the complete case study and discover the transformative power of consumer financing in the retail sector. Grab your copy now!

In conclusion, as merchants search for an efficient point-of-sale financing platform, ChargeAfter emerges as a frontrunner. Its focus on omnichannel lending and features like white-label BNPL solutions and waterfall financing ensures that merchants and consumers enjoy unparalleled experiences. In the evolving world of consumer finance and in-store financing, having a partner like ChargeAfter can be the game-changer that sets a business apart.

About Mark Denman Mark has worked in the near-prime and tertiary lending space for 30 years. As EVP of Merchants Sales & Success at ChargeAfter, he is responsible for ensuring merchants and lenders get the best care possible.

Black Friday is characterized by deeply discounted deals, early store openings, and unparalleled consumer enthusiasm, it’s been consistently marked as the busiest shopping day in America with merchants preparing for months in advance.

What is Black Friday?

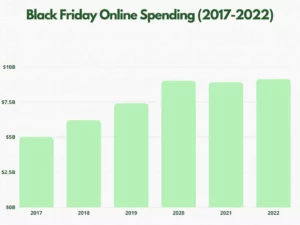

Black Friday, the day following the U.S. Thanksgiving holiday heralds the onset of the Christmas shopping season. This year it falls on Friday 24 November. In 2022 more money was spent than in the previous year with a rise in both instore and online sales.

In 2022:

In-store sales in the US increased 12% YoY (Mastercard)

Ecommerce sales in the US grew 14% YoY (Mastercard)

Global online sales on Black Friday grew by 3.5 in 2022 to reach $65.3 billion (Salesforce)

Payments made using BNPL increased by 78% (Amazon)

Why is Black Friday Important?

While the shopping spree typically extends to the subsequent “Cyber Monday” and spans an entire “Cyber Week” for many retailers, Black Friday remains emblematic. Beyond retail, this day offers an economic snapshot, a barometer for the nation’s financial health. Through the lens of Keynesian economics, which posits that consumer spending fuels economic activity, Black Friday’s sales figures can provide insights into the nation’s economic trajectory and consumer confidence.

Challenges Shoppers Face on Black Friday

Merchants meticulously prepare to cater to an influx of shoppers. This involves bolstering their eCommerce platform’s performance to prevent site slowdowns or crashes, diversifying payment options, especially with POS financing to enhance transaction success, and leveraging the efficacy of email marketing, which boasts a 4.1% conversion rate. Moreover, they strategize their discounts well in advance and prioritize a seamless online shopping and checkout experience to ensure customers enjoy an uninterrupted journey, optimizing both satisfaction and sales.

Synonymous with mega deals, Black Friday also comes with its own set of challenges for eager shoppers. One of the primary concerns is the potential for overspending. The alluring discounts and limited-time offers make deviating from a pre-decided budget easy. Shoppers might spend more than intended, especially if shopping with a credit card.

Another significant challenge is the chaotic in-store experience. Packed aisles, long queues, and overwhelming crowds can be a deterrent for many. In some cases, enthusiastic shoppers brave the cold and stand in queues for hours, only to discover that their desired product is out of stock or they get to the till only to be declined for financing.

Demand for consumer financing at the point of sale continues to rise, yet many retailers still struggle to seamlessly provide adequate financing options. Low approval rates and a subpar customer experience can result in cart abandonments, causing both frustration for the shopper and lost sales for the store.

Overcome POS Financing Challenges in Time for Black Friday

Point-of-sale financing has rapidly evolved, with consumer demands shifting and the economy showing stress. Black Friday, the shopping bonanza, is just around the corner, and merchants must be prepared to face the challenges this presents, especially with their point-of-sale financing offers. A recent survey from ChargeAfter, the embedded lending platform for point-of-sale financing, highlights the challenges that merchants face with their POS financing, including low approval rates, difficulties integrating multiple lenders, challenges with post-sale management and more.

Consumer financing is increasingly playing a strategic role for merchants as consumer demand grows. This makes perfect sense in a tumultuous economy with high inflation and soaring interest rates. For consumers, the assurance of personalized financing choices that can include spread-out payments with little to no interest, or access to other lending options such as lease-to-own, revolving credit and so on can be a beacon of hope, enabling them to commit to bigger purchases they otherwise might have foregone.

It is no longer possible for merchants to manage a robust financing offer. To provide customers with an omnichannel waterfall financing experience, they need a technology provider.

How Jerome’s Furniture Tamed Their POS Financing Challenges

Merchants who’ve recognized and adapted a platform-first approach to this trend are reaping considerable benefits. According to a case study of Jerome’s Furniture experienced a substantial uptick in sales – up a staggering 67%. These figures become even more compelling when you factor in the economic decline.

By weaving consumer financing seamlessly into their business model, Jerome’s Furniture underscored their commitment to customer empowerment and saw a surge in customer financing adoption. This indicates a vast segment of their clientele is now leveraging the store’s flexible payment options. The most commendable aspect? Despite the market turbulence in 2022 and 2023, Jerome’s Furniture maintained high approval rates, thus ensuring that customers had undeterred access to a more manageable and less burdensome financial framework.

So, as Black Friday looms, merchants have a clear strategy laid out for them: embed multiple lenders into the point of sale through an embedded lending platform. Not only does it promise to increase sales, but it also fosters brand loyalty and trust. In these unpredictable times, providing customers with financial ease can set a brand apart, making it a beacon for those looking to make the most of their Black Friday shopping.

Ready to upgrade your financing for Black Friday? Request a demo.

The contemporary financial landscape has significantly shifted towards consumer financing, driven by technology, evolving consumer behavior, and changing economic conditions. Point-of-sale (POS) financing allows consumers to purchase goods and services, especially big-ticket items, by accessing loans embedded into the customer journey. It presents an alternative to traditional financing methods like credit cards, debit cards, and cash. This rise is facilitated by embedded lending platforms like ChargeAfter, which have revolutionized the retail space by enabling businesses to offer diverse lending options to their customers.

Consumer financing products are diverse and tailored to meet the various needs of customers. These financial tools range from Revolving Credit Line and Long-Term Installment Loans to Buy Now Pay Later (BNPL), each designed to facilitate purchasing, provide flexibility in payment, or support specific financial goals. Understanding these products and finding the right fit can be essential in retaining customers and increasing sales. You can read more about the different consumer financing products available and explore the various options for POS Financing Products for retailers here.

Let’s delve into five major factors contributing to this upward trend.

1. Rising Consumer Demand Amid Inflation and Rising Interest Rates

ChargeAfter data shows that applications for POS financing significantly increased in Q1 2023 compared to the same period in 2022. This trend looks set to continue, as shoppers seek flexibility in a time of escalating prices and rising interest rates. Consumer financing is predominantly prevalent for high-priced goods and services like furniture, electronics, jewelry, home improvements, and wellness offerings. However, inflation has also driven shoppers to apply for financing for lower-cost items. This trend directly results from consumers’ necessity to maintain their purchasing power amid adverse economic conditions.

2. Aversion to Credit Card Debt Among Millennials

The fallout from the financial crisis of the early 2000s profoundly impacted Millennials, who are now more aware of the pitfalls of credit card debt than previous generations. This awareness has led to a growing interest in alternative financing options.

A recent nationwide survey by the Federal Reserve Bank of New York revealed that concerns over ongoing price inflation are causing consumers to feel increasingly pessimistic about credit access. The perception of obtaining credit is declining, with 58% of respondents stating that it’s either much or somewhat more challenging to access than just a year prior. This issue is particularly prevalent among the younger population, as 57% of millennials have reported facing challenges related to their credit scores when trying to acquire financial products.

The aversion to high-interest rates coupled with the demand for favorable payment terms has paved the way for consumer financing to become a mainstay. The prospect of predetermined monthly payments and a clear payoff date makes this option attractive, enabling consumers to manage their debt effectively without burdening traditional credit card debt.

3. Efficiency and Integration of Contemporary Checkout Financing

The modern iteration of financing has brought significant improvements in efficiency and integration. For instance, financing has been seamlessly incorporated into the checkout process, much like well-known options such as Apple Pay, Visa Checkout, and Google Pay. This integration has successfully eliminated additional steps, thus removing potential barriers to conversion. About 25% of purchases are made through consumer financing at checkout for mid to high-ticket items. The simplicity of the application process, coupled with quick financing options, enhances customer satisfaction and leads to faster checkouts.

4. Diversity of Lending Options Increases Approval Rates

Consumer financing takes many forms, providing a greater likelihood of approval for most shoppers. Those with excellent credit may opt for higher payments at a lower interest rate for a shorter repayment period. On the other hand, someone with less-than-perfect credit may prefer more flexible terms. This flexibility is made possible due to the variety of lenders available, ranging from traditional institutions to lease-to-own offers. This diverse lender network can offer approval rates as high as 85%. Access to appropriate offers at the time of purchase significantly boosts the chances of transaction completion, leading to higher customer satisfaction.

5. The Role of E-commerce and In-Store Financing

The proliferation of e-commerce has had a profound impact on the growth of consumer financing. The ability to offer flexible payment terms online dramatically enhances the customer’s shopping experience, improving conversion rates and customer loyalty. Likewise, in-store financing allows physical retail locations to provide the same flexible terms and omnichannel experience, bridging the gap between the online and offline retail experience.

The Future of Consumer Financing

The rapid growth and acceptance of consumer financing, both in-store and online, are reshaping the retail landscape. By leveraging these financing options, businesses can meet the diverse financial needs of their customers, thereby enhancing the overall customer experience and fostering long-term loyalty. Consumer financing is not merely a trend but a powerful tool that’s here to stay in the evolving world of retail.

About Mark Denman

Mark has worked in the near-prime and tertiary lending space for 30 years. As EVP of Merchants Sales & Success at ChargeAfter, he is responsible for ensuring merchants and lenders get the best care possible.

The retail industry has successfully navigated a period of uncertainty in recent years. Retailers have improved every step of the customer journey by plugging into technology to respond to challenges such as the COVID-19 pandemic and supply chain disruptions. Shoppers today enjoy a better, more personalized customer experience than ever before. We can buy goods and services online or offline, choose to have our purchases delivered in two hours or two days, buy “off the shelf” or customize our purchases – whatever suits us best.

However, during this era of inflation and high interest rates, retailers have a new struggle: providing choice and personalization in consumer financing.

The Evolving Landscape of Consumer Financing

For most of the last half-century, credit cards have been the primary solution for purchase financing. Analysis by McKinsey states that credit cards remain the most popular unsecured borrowing in the United States. Credit card borrowing accounts for 78% of balances, with a 10% growth in transaction volumes in recent years, contributing to transaction values of $49 trillion in 2021.

However, the credit card is beginning to slow as a legacy solution. Traditionally, the credit industry has worked around, rather than with, the increasing segmentation of borrower profiles. Significantly, this limitation is manifesting in the form of a demographic gap. Research commissioned by GlobalData revealed a marked rise in the percentage of under 35s not possessing a credit card — 47% in 2022, compared to 39% in 2016.

Instead, younger and underserved shoppers are adopting point-of-sale loans embedded in the customer journey as an alternative to credit cards. These demographics enthusiastically embraced Buy Now Pay Later (BNPL) as an attractive alternative for consumer financing. BNPL offers convenience through competitive APR rates, predictable repayment schedules, and flexible approval requirements. However, it has its limitations. Originating from the fintech industry, new regulations by the Consumer Financial Protection Bureau threaten BNPL providers as loan defaults grow.

Additionally, this type of loan is only suitable for small-ticket items. Shoppers need an alternative to finance big-ticket purchases such as furniture, electronics, home improvement, jewellery, etc. And while plenty of other lending products are available for these purchases, retailers struggle to offer their shoppers a choice of financing options at the point of sale.

The Challenges of Existing Embedded Lending Frameworks

Embedded lending is experiencing rapid growth, with market revenue reaching US$4.7 billion in 2021 and projected to rise by US$32.5 billion in the next decade. However, given the complexity of embedding multiple lenders into omnichannel customer journeys, currently, most retailers offer a single-lender solution.

This single-lender model limits retailers’ ability to provide financing options that cater to their customers’ needs and preferences. Lenders typically specialize in specific financing products, such as installments, 0% APR, BNPL, lease-to-own, etc., targeting specific customer segments – prime, near-prime, or subprime. This limited financing focus leads to poor approval rates, abandoned carts, lost sales, and customer dissatisfaction. Furthermore, relying on a single lender exposes retailers to the risk of changing lending conditions, especially as lenders tighten their underwriting strategies and approve lower approval rates and transaction values.

Retailers know this, and many attempt to integrate a second lender into their offer. However, this approach results in a heavy lift for the retailer and a poor and fragmented experience for the customer.

However, this is changing. The technology enabling retailers to embed multiple lenders into omnichannel customer journeys is now available.

An increasing number of retailers are embracing a platform-first approach to point-of-sale financing.

Unlocking the Potential of Embedded Lending in Customer Journeys

Given the difficulties in managing multiple lenders, retailers are adopting a platform-first approach quickly. ChargeAfter’s embedded lending platform enables retailers to easily configure a waterfall of lending options that address all credit profiles from credit-invisible to super-prime and everything in between into omnichannel customer journeys.

This model benefits all of the players in the ecosystem. Retailers offer flexible financing options to customers at their moment of need, resulting in up to 85% approval rates, increased sales, higher average order value (AOV), and improved customer satisfaction and loyalty. Shoppers access financing choices from trusted lenders, enabling them to purchase the goods and services they desire with the terms and conditions that best suit their needs and preferences. Lenders, in turn, gain direct access to customers needing their services. This comprehensive solution creates a win-win-win situation for the entire consumer financing ecosystem.

Kevin has worked in the banking and finance industry for over a decade. He has worked closely with some of North America’s largest banks and financial institutions and retailers. Kevin is an expert in embedded consumer financing, with a deep understanding of current trends and where the industry is heading.

By expanding its network of lenders to include Wells Fargo, ChargeAfter enables merchants to provide their well-qualified consumers with fast approvals.

NEW YORK, August 16, 2023ChargeAfter, the embedded lending platform for point-of-sale financing, announced today that it is partnering with Wells Fargo Retail Services, a division of Wells Fargo Bank, NA that facilitates the delivery of consumer private label and industry credit card programs to retailers.

Merchants that use ChargeAfter’s platform to provide point-of-sale financing will now be able to offer their consumers Wells Fargo’s private label credit programs. Wells Fargo’s private label credit programs are designed to serve consumers with extended promotional terms and fast approvals for qualified consumers. These financing options are critical to retailers and service providers that operate in home goods, home improvement, outdoor living, jewelry, etc. Consumers can access the Wells Fargo private label credit product through a fast and frictionless embedded process at the point of sale.

Steve Jermier, Senior Vice President of Relationship Management for Wells Fargo Retail Services stated,“Partnering with ChargeAfter enables us to easily embed our private label card products into the merchant’s point-of-sale. ChargeAfter’s simple integration into e-commerce and in-store POS platforms provides consumers with quick and convenient access to our product. This allows our retailers to provide consumers with financing for their individual needs at any point of sale.”

Meidad Sharon, CEO of ChargeAfter commented, “We are delighted to partner with a global banking leader such as Wells Fargo. Integrating Wells Fargo’s private label credit products into the ChargeAfter platform enables merchants to easily provide consumers with fast access to the best financial choices available. As embedded lending becomes the new standard for merchants’ checkout experience, our platform maximizes customer buying power where it matters most – at the point of sale.”

About Wells Fargo Retail Services:

Wells Fargo Retail Services, a division of Wells Fargo Bank N.A., facilitates the delivery of consumer private label and industry credit card programs to retailers, manufacturers, distributors, associations, and buying groups in a variety of markets. Learn more at wellsfargo.com/newbusiness.

About ChargeAfter ChargeAfter is pioneering the embedded lending network for point-of-sale consumer financing for merchants and financial institutions. Powered by a network of lenders and a data-driven matching engine, ChargeAfter streamlines the distribution of credit into a single, secure, and reliable embedded lending platform. Merchants can rapidly implement ChargeAfter’s omnichannel platform online, in-store, and at every point of sale, enabling them to provide personalized financing choices to their customers.

ChargeAfter is backed by payment expert investors including Visa, Citi Ventures, Synchrony Financial, Banco Bradesco, MUFG, PICO Venture Partners, Propel Venture Partners, and The Phoenix. ChargeAfter is headquartered in New York with an R&D center in Tel Aviv. Learn more at chargeafter.com